Description

Two-Steps Benchmarks for Time Series Disaggregation.

Description

The twoStepsBenchmark() and threeRuleSmooth() functions allow you to disaggregate a low-frequency time series with higher frequency time series, using the French National Accounts methodology. The aggregated sum of the resulting time series is strictly equal to the low-frequency time series within the benchmarking window. Typically, the low-frequency time series is an annual one, unknown for the last year, and the high frequency one is either quarterly or monthly. See "Methodology of quarterly national accounts", Insee Méthodes N°126, by Insee (2012, ISBN:978-2-11-068613-8, <https://www.insee.fr/en/information/2579410>).

README.md

![]()

![]()

Overview

The R package disaggR is an implementation of the French Quarterly National Accounts method for temporal disaggregation of time series. twoStepsBenchmark() and threeRuleSmooth() bend a time series with another one of a lower frequency.

Installation

You can install the stable version from CRAN.

install.packages("disaggR")

You can install the development version from Github.

# install.packages("devtools")

install_github("InseeFr/disaggR")

Usage

library(disaggR)

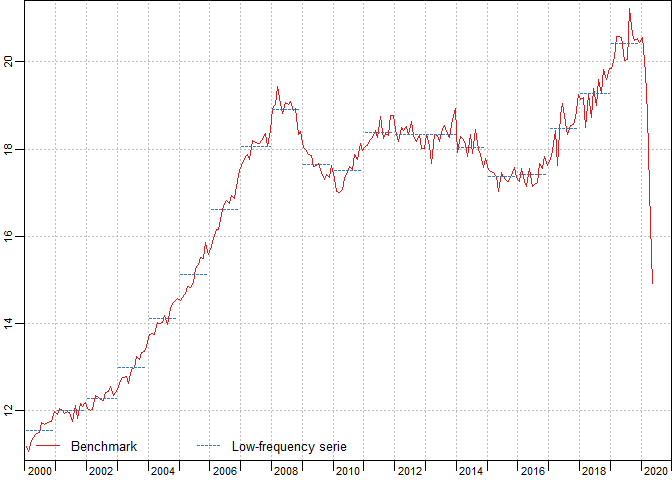

benchmark <- twoStepsBenchmark(hfserie = turnover,

lfserie = construction,

include.differenciation = TRUE)

as.ts(benchmark)

coef(benchmark)

summary(benchmark)

plot(benchmark)

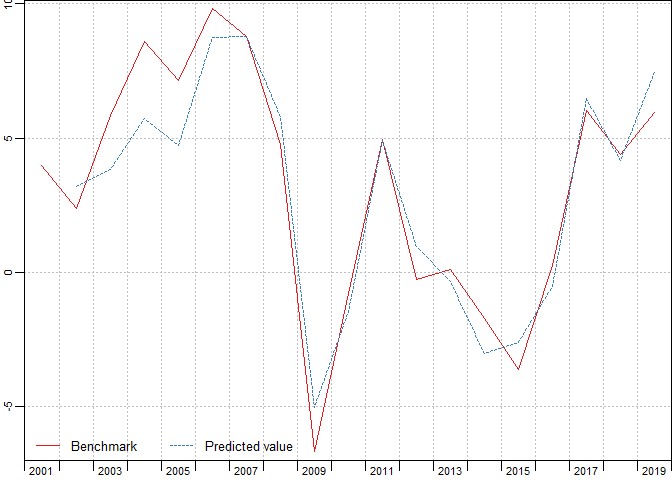

plot(in_sample(benchmark))

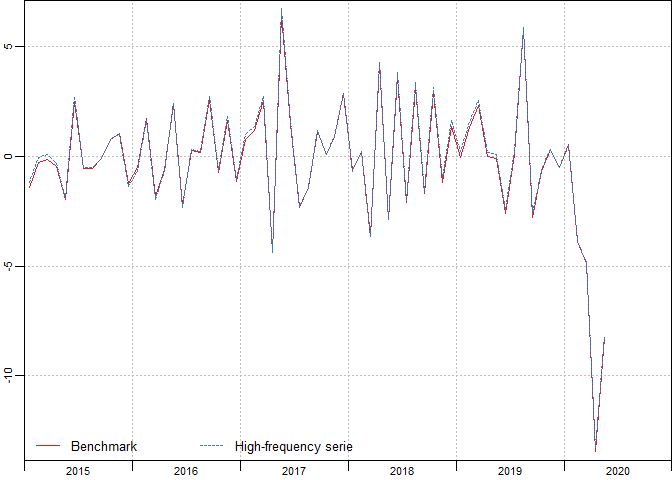

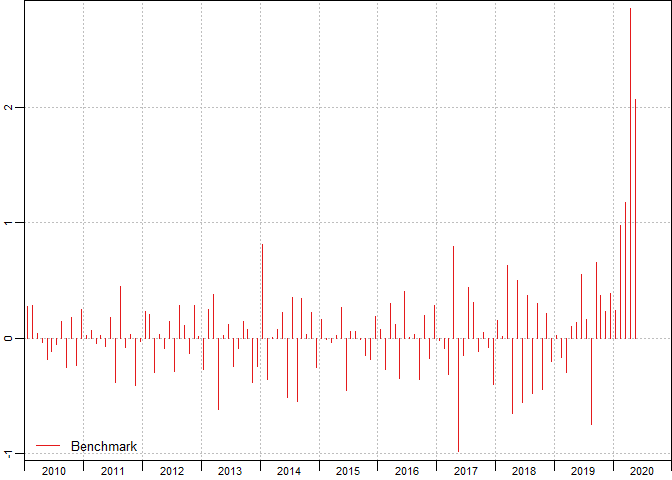

plot(in_disaggr(benchmark,type="changes"),

start=c(2015,1),end=c(2020,12))

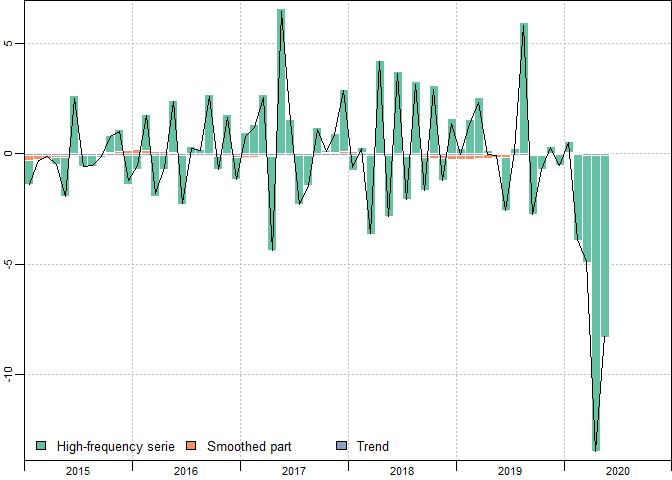

plot(in_disaggr(benchmark,type="contributions"),

start=c(2015,1),end=c(2020,12))

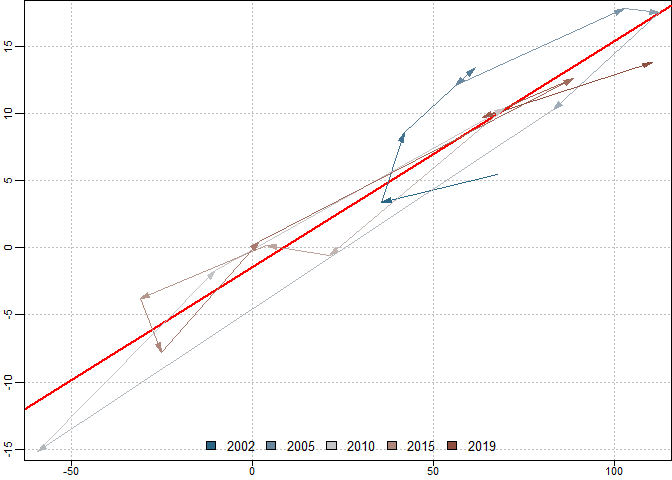

plot(in_scatter(benchmark))

new_benchmark <- twoStepsBenchmark(hfserie = turnover,

lfserie = construction,

include.differenciation = FALSE)

plot(in_revisions(new_benchmark,

benchmark),start = c(2010,1))

Shiny app

You can also use the shiny application reView, to easily chose the best parameters for your benchmark.

reView(benchmark)